How Solar Fits into Your Rural Real Estate Wealth Transfer Strategy

Most conversations about rural solar focus on monthly bills and energy reliability. But there's a longer game most haven’t considered: what that system means when the property transfers to the next generation.

A functioning, grid-independent or off-grid solar and battery system in a rural property doesn’t just solve your current energy challenges. It’s also a durable infrastructure asset to a piece of real estate that a spouse, child, or grandchild will eventually own, live on, or sell.

Here’s how to maximize the advantage of adding solar to your rural property as part of your estate planning strategy.

Rural real estate can throw a monkey wrench into the great wealth transfer

Baby boomers currently hold approximately $19.7 trillion in U.S. real estate, representing 41% of total national property value. Among millennials and Gen Z expecting an inheritance, 62% anticipate receiving real estate, such as a primary residence, a vacation property, or land.

Rural properties are often the most meaningful assets a family owns. However, they’re also the most complicated to pass down. Remote location, operational complexity, high carrying costs, and limited buyer pools can turn an inheritance into a burden rather than a windfall.

Many factors determine how this legacy is perceived and handled, with the energy infrastructure playing a significant role. A robust solution that supports hassle-free modern living, stops power bills from being an ongoing drag, and makes outages a non-issue means your grandchild won’t say, ”Grandpa, what pickle have you put me in?!”

Solar boosts property value, with caveats

A SolarInsure study analyzing 5,000 California home sales between 2020 and 2023 found that homes with owned solar sold for 5–10% more than comparable non-solar ones. Meanwhile, homes with leased or third-party-owned solar (i.e., PPAs) saw no premium at all.

Per Freddie Mac's updated guidelines, effective August 2024, solar adds appraised value only when the system is owned. Leased systems and PPAs don't count, and they don’t contribute to your property's appraised value — the panels may actually transfer as a liability.

That added value is critical to the wealth transfer conversation because appraised value at the time of transfer sets the step-up in basis for your heirs.

Meanwhile, the type of solar matters, especially in rural environments. Unlike grid-tied solar systems, which are vulnerable to outages and rate increases, grid-independent or off-grid solar systems eliminate utility dependence because they run whether the grid is up or not.

Off-grid solar also represents a cost saving that doesn't show up in typical comps. Extending electric service to rural property averages $10,000–$30,000, depending on distance from the grid. Rural California terrain, fire risk zones, and distance from existing infrastructure often result in significantly higher costs. Having an energy infrastructure on your property will eliminate the expense and headache for your heirs.

However, off-grid and grid-independent solar isn’t often well-understood by most appraisers. To ensure your property is valued favorably, prepare a complete system disclosure package with clear specs and performance history.

California property tax incentives for solar

California has long offered a property tax incentive for solar. Under Revenue and Taxation Code §73, adding a qualifying active solar energy system to an existing property is excluded from new construction assessment — meaning your assessed value doesn't increase because of it. (Always verify with your county assessor to ensure that your system qualifies.)

However, this exclusion sunsets January 1, 2027. A system implemented before the deadline keeps your assessed value flat for as long as you own the property — a benefit that can span decades. At transfer, the solar system's value becomes part of the new assessed value, which your heirs inherit as their new tax base.

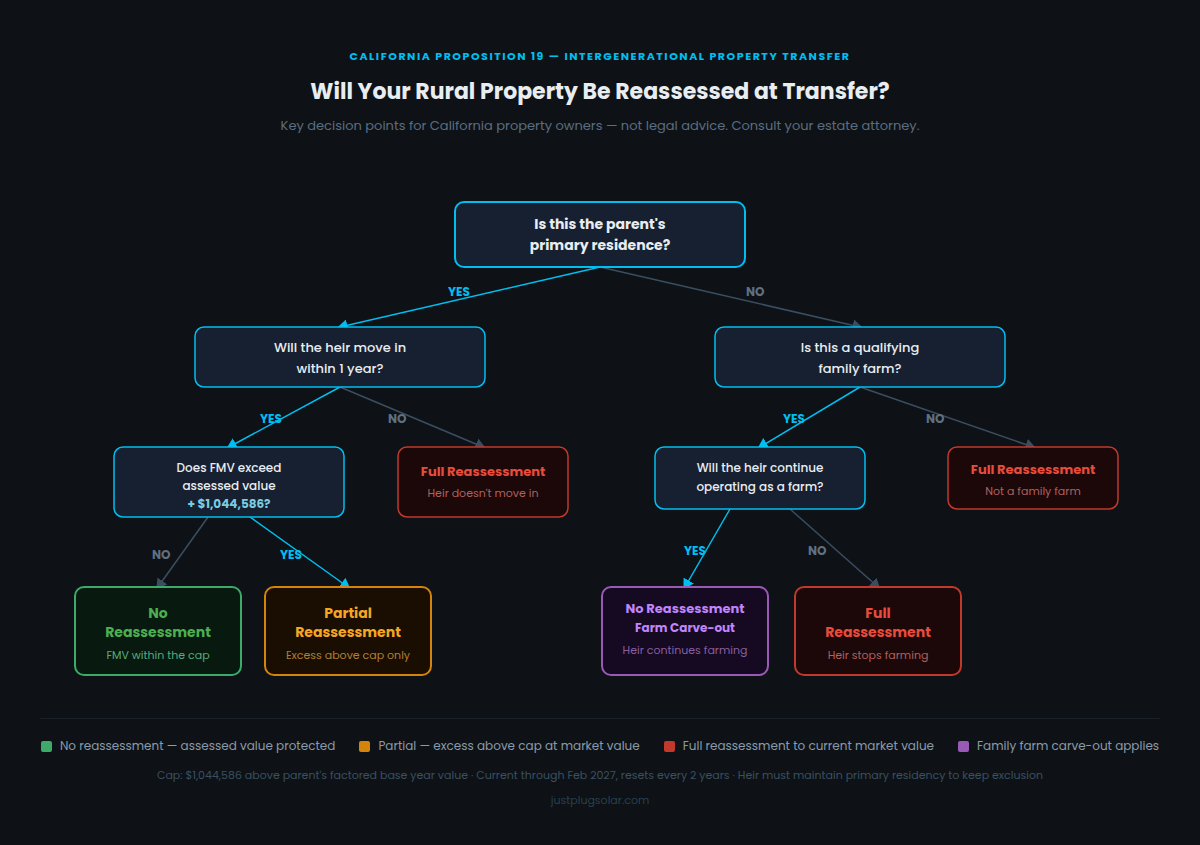

How Prop 19 changes intergenerational property transfer

Before Prop 19, which went into effect in February 2021, California parents could transfer any property to their children without triggering a reassessment to the current market value. The child inherited the parents' low assessed value and property tax bill, regardless of how they use the property.

Prop 19 has removed that broad exclusion. The exclusion now applies only to a primary residence. The heir must move into the property within one year of inheriting it and file for the homeowners' exemption. Rental properties, vacation homes, and investment properties no longer qualify and are reassessed to full market value at transfer.

Moreover, the applicable exclusion is capped. The heir can maintain the parent's assessed value only up to the parent's factored base year value plus the current indexed amount ($1,044,586, effective through February 15, 2027). Any value above that cap is reassessed.

What Prop 19 means for rural property owners

The scenarios vary significantly depending on how your property is classified and what your heir intends to do with it.

If the rural property is the parents’ primary residence and an heir moves in within the required window, a meaningful exclusion is available. Whether it fully protects the assessed value depends on the math: a property worth $700,000 with the parent's factored base year value of $150,000 might transfer with little to no reassessment. For a property worth $3 million, the excess above the cap will be reassessed.

If the property is a second home, a rental, or an investment property, even if the family has owned it for generations, it’s fully reassessed to the current market value when it transfers. That can mean a substantial increase in annual property taxes.

The family farm carve-out

Family farms have a separate provision under Prop 19. Qualifying transfers can be excluded from reassessment if the heir continues to use the property as a family farm. If your rural property qualifies as a family farm under California's definition, that's a different conversation than the residential exclusion and potentially a more favorable one. Ask your estate attorney specifically about this.

How solar fits into the Prop 19 picture in estate planning

The connection between solar and Prop 19 runs in two directions — assessed value and carrying costs — and they often pull the numbers in different directions. Here are a couple of scenarios:

If the property is a second home or investment property

Under Prop 19, there is no exclusion for second homes, rentals, or investment properties. The property is reassessed to the current fair market value (FMV) at transfer. The CA property tax exclusion under R&T §73 protects the owner's assessed value from rising while they hold the property. However, it only belongs to the original owner.

The property transfer triggers reassessment, and the heir's new tax base reflects full current market value. A solar system that added to the property's appraised value during the parent's lifetime becomes part of that reassessed value at transfer.

If the heir moves in and claims the primary residence exclusion

If the property's FMV at transfer falls below the parent's assessed value plus the $1,044,586 cap, no reassessment occurs. If FMV exceeds that threshold, only the amount above it gets reassessed.

A solar system that increases a property's appraised value increases the FMV, which can push more of the property's value above the cap and into partial reassessment territory. That's the potential exposure. However, two things offset it.

First, that higher FMV becomes the heir's step-up in basis, reducing capital gains exposure if they eventually sell (more on this in the next section).

Second, a low utility bill (for a grid-independent system) or no utility bill at all (for an off-grid solution) offsets the higher property tax bill. The heir will not need to worry about skyrocketing utility bills for years to come or paying tens of thousands for a grid connection.

The heir must continue occupying the property as their primary residence to maintain the exclusion. If they move out, the assessed value adjusts to reflect market value as of the date of inheritance, plus allowable annual increases.

This section describes general legal concepts, not legal advice. Ask your estate attorney how Prop 19 applies to your specific property, including its classification, current value, and how it's titled, as all affect the outcome.

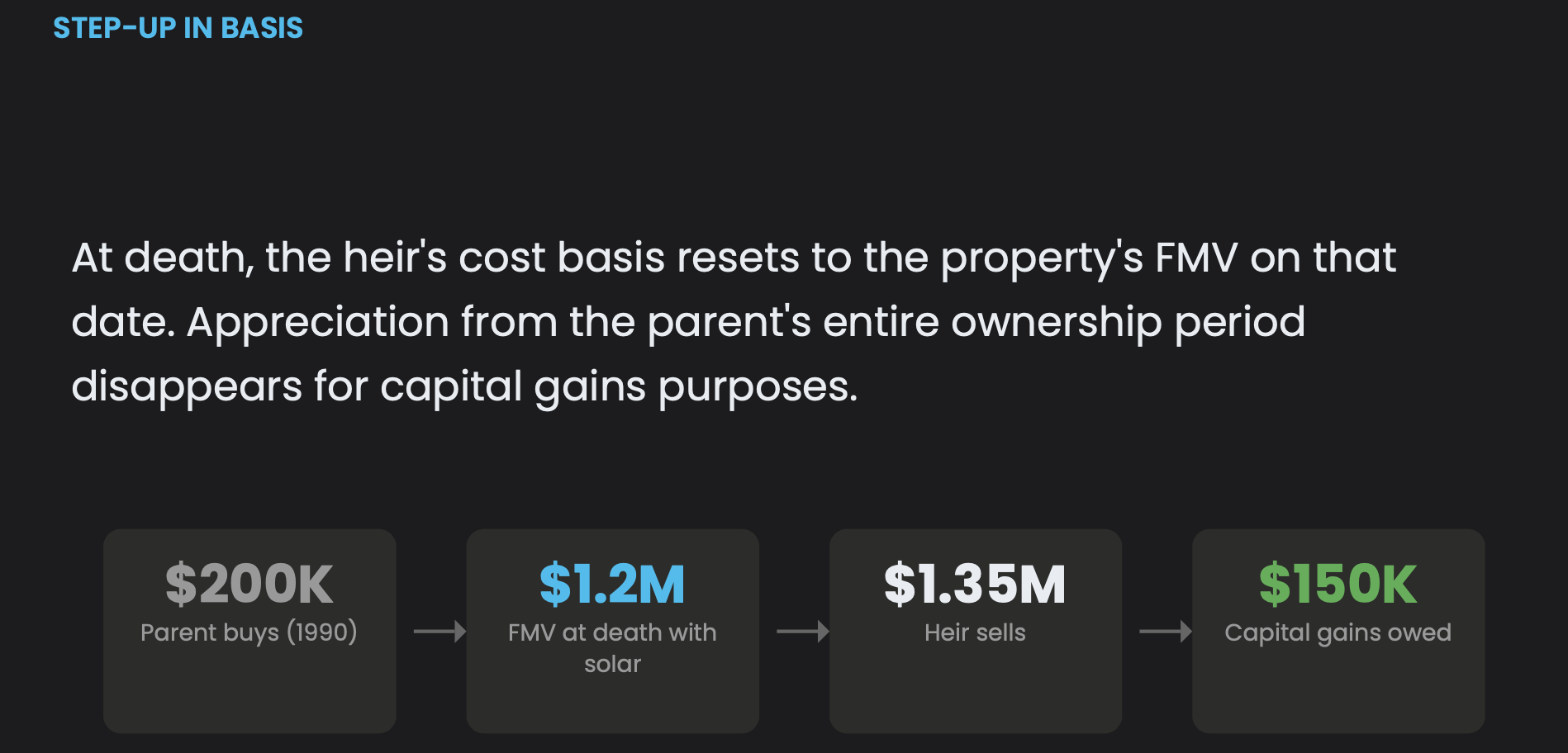

What the step-up in basis means when the property eventually sells

Per the step-up in basis under IRC §1014, when a property transfers at death, the heir's cost basis for capital gains purposes resets to the property's FMV on the date of death.

An heir only owes capital gains tax when they later sell the inherited property, and only on appreciation that occurred after the date of inheritance — not during the original owner's lifetime.

For example, a parent bought rural land for $200,000 in 1990. They implement an off-grid solar system, document and maintain it well, and the property appraises at $1.2 million at death. The heir's cost basis is $1.2 million. If they sell two years later for $1.35 million, capital gains are owed on $150,000, not $1.15 million.

The solar system is part of that $1.2 million appraised value, assuming it's been documented for appraisal purposes. A system that adds to the property's value reduces the heir's eventual capital gains exposure without any planning acrobatics.

Step-up in basis rules can be affected by how a property is held, e.g., through a trust, a will, or direct transfer, and by other factors specific to the estate. Consult a tax professional or estate attorney for guidance on your situation.

Consider power costs from your heir’s perspective

The challenges of rural living, such as navigating outages, the sticker shock of high power bills, and jumping through hoops to hook up an off-grid property, may deter your heir from staying in or keeping the property.

Passing down a property with grid-independent solar means your heirs won’t inherit high power bills, exposure to rate increases, or frequent, prolonged outages.

Meanwhile, an off-grid property with a robust solar solution means your heir doesn’t have to worry about the cost of a utility line extension, which could be tens of thousands of dollars, or make do with a generator set up that’s noisy, costly, and potentially fire-prone (if not set up properly). Instead, they will inherit a property ready for modern living without the hurdle that could prevent meaningful use.

If your heir isn’t ready to or decides not to move into the property, a solar solution lowers the carrying cost (i.e., the cost to maintain the property while it sits), allowing them the breathing space to make a thoughtful decision about the next step.

Maximize the tax benefits and lower the energy burden for your heir

Let’s revisit Prop 19 in the context of solar.

A large solar system may significantly increase a property's appraised value, pushing the FMV at transfer above the Prop 19 cap and increasing your heir's property tax base. Although R&T §73 keeps your assessed value flat while you own the property, that protection doesn't carry through to the heir.

A thoughtful solar strategy can help you balance property value with the ease of transitioning by strategically right-sizing the system based on your current usage and wealth transfer strategy.

Your calculus should also account for the savings you gain during the years between implementing the system and passing the property to your heir. With a modest grid-independent solution, most of our clients achieve a 5-year (or less) payback time. That means if you use the system yourself for 5+ years before passing it on, you’ve already made your money back, and the rest is gravy.

Additionally, consider a grid-independent or off-grid solar solution as energy infrastructure and factor in the cost of outages and the peace of mind that the property runs whether the grid is up or not. As Public Safety Power Shutoff (PSPS) events become more frequent and lengthy, energy resilience is more critical than ever in rural regions.

Whether you’re implementing grid-independent or whole-property off-grid solar, we can help you engineer a solution for your current needs without excessive capacity. This will help keep the initial investment modest and avoid unnecessarily inflating the property value.

Moreover, we may involve your heir in the discussion and explore how they plan to expand the system. Our solutions incorporate scalability and expandability from the start, so they can grow to meet evolving needs when the time is right.

Let’s talk through what makes sense for your situation and design a plan.