Grid-Independent Solar Financing Options for Rural Property Owners

We’ve been conditioned to pay utilities every month and (usually) get electricity in return. It’s like paying rent — you have no equity, ownership, or hedge against rate increases. But nobody questions whether it has to work this way.

Well, it does not. We’ve reached the tipping point in solar technology where an off-grid or grid-independent solar solution is reliable and affordable enough for us mere mortals to challenge “how things are done.” We can now flip the script on who controls our energy independence.

This is especially true for rural property owners, who have been at the bottom of utility’s priority list — receiving poor services, tolerating frequent, prolonged outages, and having no say in their skyrocketing power bills.

Grid-independent solar is the way to go if you have an existing grid connection and want to build energy resilience while lowering your monthly bill. But coming up with that good chunk of change isn’t trivial. Here’s what you need to know about your financing options.

What is grid-independent solar?

Grid-independent solar is not the same as a standard grid-tied solar system, which works within the utility’s system and rules.

In a grid-tied arrangement, your panels generate power, but the utility controls the terms: it dictates what you get credited for the power you export and determines your rate for the power you draw back at night.

When the grid goes down, your system doesn’t produce power. Even though you have solar, you’re still fundamentally a utility customer.

Grid-independent solar follows a different architecture. Solar panels and a battery bank are your primary power source. The inverter routes power to your house first, stores surplus in the battery, and draws from it when solar production falls short at night or on overcast days.

The utility grid stays connected as a low-cost backup for the rare times you need it (e.g., when you use high-draw/high-surge appliances or during long stretches of overcast days). The property runs on your own energy infrastructure the vast majority of the time — if the grid goes down forever, you’ll be just fine.

The most critical mindset shift behind the energy independence revolution

Most people treat solar as an expense rather than an investment. This framing may work in a typical suburban setting, but it leads rural property owners down the wrong path when a grid outage has far more at stake than a few hours without WiFi or a small fridge’s worth of spoiled food.

Instead, you should compare owning your energy infrastructure vs. renting it indefinitely from a utility. Here’s why:

Infrastructure has different economics than a purchase. It’s designed, right-sized, documented, and maintained with a known performance baseline and a service history. It produces value continuously, not just at the moment of sale. Additionally, it allows you to develop your land the way you want and boosts property value.

Consider your energy system like you do a well, a septic system, or a road. It’s not like, for example, a bread-making machine. It’s the foundation on which your property operates.

Does financing an energy infrastructure make financial sense?

If you’re paying your power bill, the money leaves your account every month anyway. Wouldn’t it be better to use it to pay for an asset that you own and control? Once you frame grid-independent solar as infrastructure, you’d realize that you’re not adding a new expense but turning an expense into an investment. Boom.

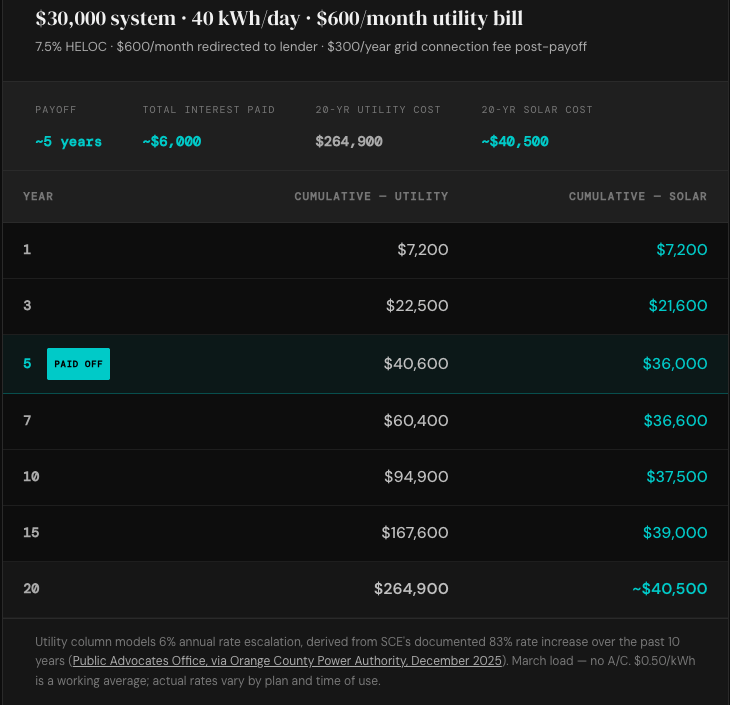

But the math still needs to work. Here’s how it pencils out for a typical household using 40 kWh/day at a blended rate of around $0.50 per kWh:

The household pays a monthly electricity bill of around $600. Over 20 years, including an annual increase of about 6%, they will hand over roughly $265,000 to the utility… and own nothing.

If you finance a grid-independent solar solution with a loan, such as a home equity line of credit (HELOC), you redirect that same monthly payment of $600 toward an asset you own instead of paying the utility company.

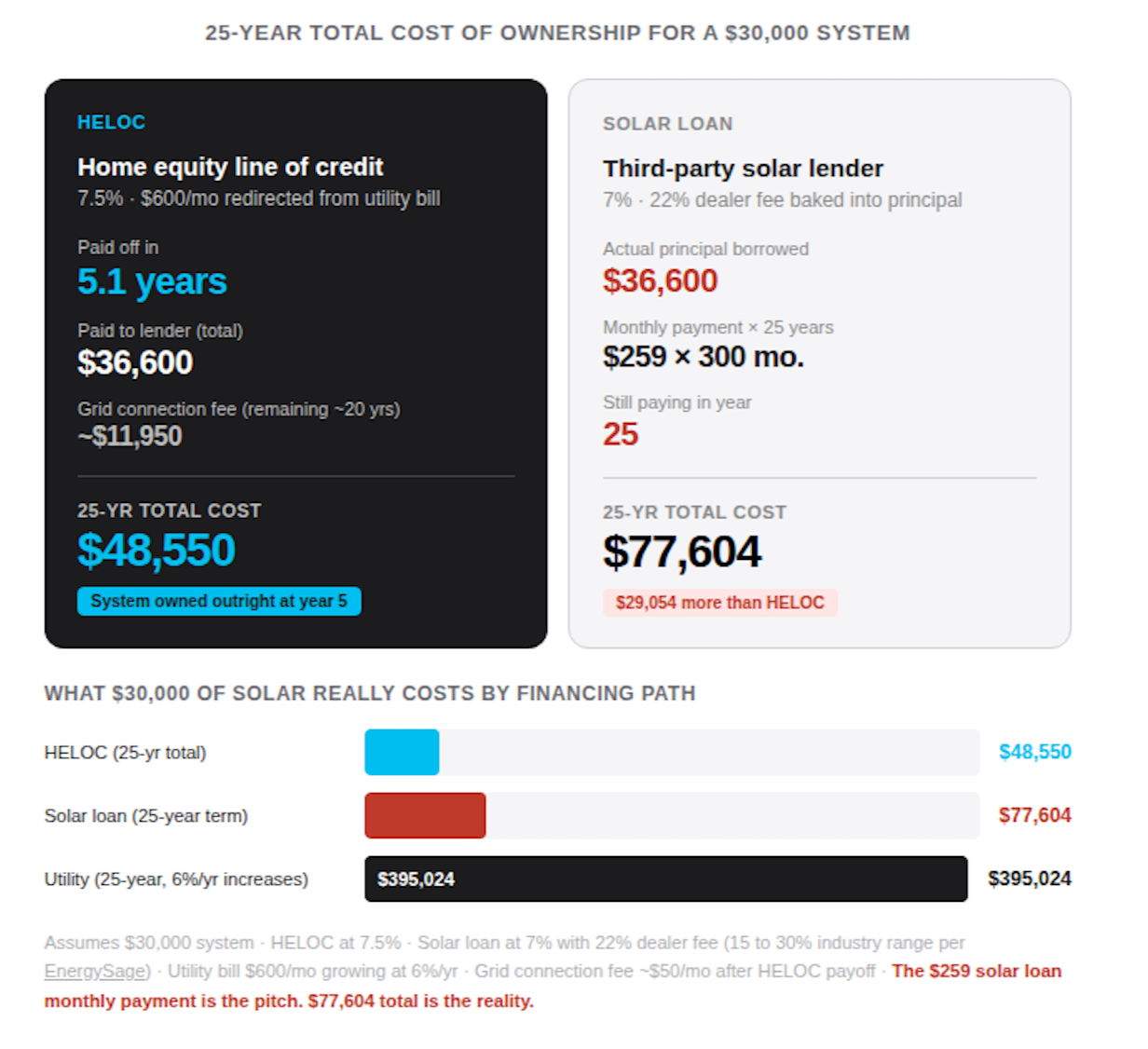

Let’s assume a $30,000 grid-independent solar system (quite typical for our clients), financed at 7.5% — close to the current national average adjustable HELOC rate of 7.21% (Curinos, May 2026; rates vary by lender, credit profile, and loan-to-value ratio, so verify current rates when you apply). The total cost of ownership over 20 years, including ongoing grid connection, maintenance, and monitoring costs, is ~$54,000.

$265,000 vs. $54,000. Mic drop.

>> Use our Solar Payback Time Calculator to run your numbers.

Why a HELOC beats a “solar loan” when independence counts

At first glance, solar loan rates look competitive. Best-in-class credit union solar loans typically offer an interest rate of 6.25 to 8.00% APR. Some solar-specific lenders advertise rates as low as 1.99%. On paper, those numbers may look better than a HELOC. But you must go beyond rate comparison and understand what’s built into those loan agreements.

In 2026, solar loans routinely include dealer fees of 15 to 30% baked into the loan principal, inflating your balance by thousands of dollars. The advertised low APR is no longer low because of that hidden markup, and the effective rate is much higher than the headline number.

On a $30,000 system, a 22% dealer fee means you are actually financing $36,600. How much that hurts depends on the loan term:

At a 7-year term, the monthly payment is $552, with a total of $46,401 paid to the lender. Compare that to a 7.5% HELOC, which totals around $36,600 and is paid off in 5.1 years. At a 10-year term, the monthly solar loan payment drops to $425, but the total amount paid rises to $51,000 — you’re still writing checks four years after the HELOC is retired.

At 25 years, the monthly drops to $259 — and that’s the number sales reps lead with. But here’s the catch: the total you pay the lender goes up to $77,604. That’s $29,000 more than the HELOC, and it’s offered (and promoted and pushed) because low monthly cost closes deals.

Bottom line: a HELOC is your equity from your bank on your terms. You don’t have to worry about a solar company sitting on your title or a dealer fee inflating the balance. You pay it off, and the system is yours — free, clear, and encumbrance-free.

One more thing worth knowing: the 30% federal residential solar tax credit (Section 25D) expired December 31, 2025. Lease and PPA companies, however, still qualify for the commercial Section 48E tax credit through 2027. They claim the tax credit, not you.

As a result, we can expect the lease and PPA pitch to get even more aggressive and sneaky (if that’s even possible…). The economics of those arrangements have always favored solar companies, and now, that gap has widened even more.

A note on California's GoGreen Home program

California's GoGreen Home program offers attractive rates and has no dealer fees. However, there’s a catch. The program requires work to be completed by contractors from its approved network, and loan proceeds go directly to them.

Here’s the rub: the program is administered in partnership with California's major investor-owned utilities, namely PG&E, SCE, SDG&E, and SoCalGas. The approved contractor network reflects that partnership, and the contractors operating within it are almost certainly working within the grid-tied solar framework.

The program's own eligibility language reveals the intention:

The Battery Storage EEM for adding storage to an existing solar system explicitly requires NEM enrollment on the electric bill. NEM enrollment means you’re on a utility net metering arrangement, which is grid-tied by definition. The Bundled Solar + Battery EEM does not specify grid-tie, but the broader program eligibility requires the property to receive service from an investor-owned utility or Community Choice Aggregator. As such, the grid relationship is baked into property eligibility.

In plain English, you’ll most likely get a system that depends on the utility. While the financing may be cheaper, the outcome doesn’t give you energy resilience: your power goes off during an outage, and you’re still at the utility company’s mercy.

Why does it matter now more than ever? Here’s a cautionary tale:

Liberty Utilities, which serves roughly 49,000 rural Californians across Placer, El Dorado, and five other Sierra Nevada counties, will lose 75% of its power supply in May 2027 as NV Energy is redirecting that capacity to data centers.

It’s an extreme case, but the underlying dynamic is not unusual: rural customers sit at the back of the queue when utilities make resource allocation decisions. A state-backed loan program designed and administered by those same utilities is unlikely to benefit consumers at the expense of their revenue and profitability.

This takes us back to a HELOC, which gives you complete control over your financing situation. But there’s more to it than choosing the right financing structure.

Expert engineering is the first step to smart financing

Here’s the caveat: the financing math won’t work in your favor (as much) if you pay $300 a month in power bills but are sold a $70k system. The key to maximizing your investment starts with engineering a solar solution that meets almost all your needs without paying for capacity you rarely use or don’t use at all.

But that’s not how most solar providers work.

A standard grid-tied solar quote is largely a function of a customer’s average monthly bill and whatever the installer has in stock. The goal of the utility and vendor is to maximize year-round yield because they can sell whatever you generate but don’t use to your neighbors at the full retail rate. They don’t care how your usage distributes across the day, which loads are flexible and which are not, how you plan to grow your ranch, or how your terrain affects production.

They size your system to a rough average, and if it underperforms (e.g., they don’t care if your roof is pointing the wrong direction), you pay for grid power to cover the gap. That means you have to pay for the loan and the power bill!

Here’s how our nerd (ok, ok, engineering)-forward approach differs:

Before any system design, we discuss your usage patterns: what you run, when you run it, how that shifts seasonally, and how you plan to grow. We analyze the site to understand its actual production potential, and shape the design based on context (e.g., even how far the buildings are apart and from the electrical panel can affect the system design).

Overbuilt systems cost more upfront and inflate a loan accordingly, pushing out the payback timeline and reducing the financial case for going solar. However, the opposite will also cost you: a system that’s too small flips to grid power more often than it should, and you still have a power bill to pay.

To maximize your investment, we engineer a system that covers your needs without building in excess capacity you will pay for but rarely use.

We typically dimension a system to handle 90-95% of the day-to-day load while keeping the grid connection as a low-cost backstop for edge cases, such as a long stretch of overcast days, a large seasonal load, or that welder you use 2.3 times a year.

Paying for the equipment to support those scenarios in your primary system makes no financial sense when the grid connection, already paid for, can handle them at minimal cost.

Let’s run the numbers for your property

Every property is different. Your bill, usage pattern, equity position, and growth plan all affect what the right solution looks like and how the financing math works. We consider all of those from your point of view, without ties to any lenders that muddle the picture. If you want a straight answer on what makes sense for your situation and what the numbers look like, let’s talk.

No matter your energy situation, we have a solution to boost your energy resilience:

You’re a current utility customer with no solar ➡️ start here.

You have grid-tied solar, but the bills and outages aren’t working out for ya ➡️ start here.

You have an off-grid property and want to stay off-grid without compromise ➡️ start here.